Have you missed out on any loan EMI? Yes? You are still not a loan defaulter. Well, you are technically speaking, but that’s just as per the textbook definition. There is a scope of redemption.

Who is a Loan Defaulter?

Missing out on even one EMI payment makes you a defaulter. However, debt collection is an expensive process for banks. Hence, they offer a grace period post due date to pay your EMI. There are late payment charges/fees (charges may vary) levied by the banks depending on the nature of your loan. In case you miss payments frequently, then the bank will enforce a default provision in the contract.

| Loan Type | How long until default after the last payment? | Grace Period |

| Credit Card | 180 days | 3 days allowed before late payment fees |

| Auto Loan | 90 days | At least 30 days but varies from bank to bank |

| Education Loan | 90 days | Repayment commences after 1 year of completion of education or 6 months from joining a job, whichever is earlier. |

| Mortgage | 150 days | 90 days |

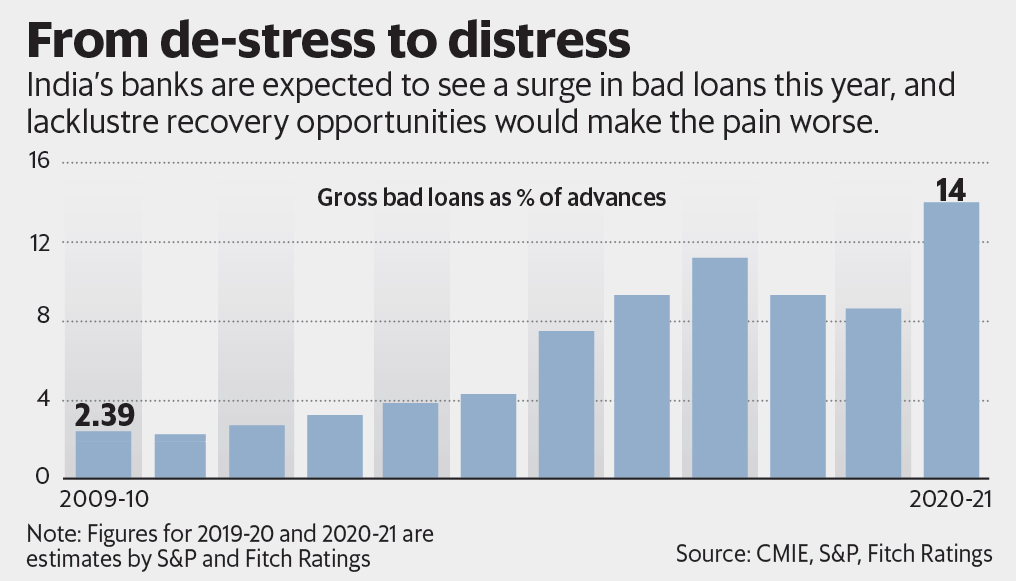

It does not mean that missing out on EMIs is to be taken casually. However, repayment of loans and keeping up with the EMI’s is a daunting task, particularly when you feel you‘re already drowned in debt. Current COVID-19 situation is paving the way for the rise in delinquencies and delays in debt recovery; leading to a grave economic turmoil.

Wilful defaulters have been rising much before the lockdown; so much so that lenders have filed cases to recover debt amounting to nearly Rs.25,000 crore. Financial indiscipline will bite us later- on a macroeconomic front as a nation and a micro-level as an individual. Even though it might seem that the ship has sailed, and nothing can be done except pretending that your debt doesn’t exist, there is a lifeboat around. It might not only save you from your debts but also bring back your financial life on track. Should you prefer to take the lifeboat than drowning in debt, that is!

Firstly, understand that missing out on successive EMIs does not mean you will lose the ownership of your asset at once. You have time until the situation stoops to this- Negotiate with the bank.

Will the bank negotiate? Do banks negotiate?

Yes! Banks are equally concerned (or maybe more) when you miss out on your EMIs, which translates to a potential NPA/Bad debt in their books. Hence, if you get in touch with them, they are most likely to help you than resist you.

As a debt counselling agency, this is what we do for EMI defaulters for free. Here, we share a few tips and tricks from our years of experience on how to negotiate with the bank correctly.

Get in touch with the bank- This is the first and foremost tip! Most people shy away from confronting the bank and explaining their genuine problems because of which they are not able to pay their EMIs duly. In such a scenario, consider the bank as your ally, and not an enemy. Most probably they will come up with a common ground on which you can confidently stand, and avoid being a defaulter as well.

Below are a few primary areas you can revisit the bank during your negotiation:

- Increase loan repayment tenure: This will lower the monthly instalment payment. However, the interest payout will go up. Hence, increase your EMI amount as soon as your financial situation improves. Beware of a few banks or NBFCs that levy hidden penalties/charges for delay in payments.

- Restructure the loan: Renegotiate the terms and conditions of the loan – lower interest rate, loan tenure, moratorium or interest payments. You can also consider giving assets like gold, PPF, or a house as additional collateral for reducing EMI.

- One-time settlement: If the interest accrued is higher than the principal amount, opt for a one-time settlement. An easy way out to clear your loan off the books provided you have enough assets to repay. It is case-specific, and the settlement amount is lower than the original amount. Bank may

- EMI Holiday: it means requesting the bank in advance for a relaxation period to pay your EMIs. If you foresee a financial situation, then seek temporary EMI relief, or an EMI holiday to set things right. Banks permits deferment to genuine customers. However, you may need to pay additional interest that can be negotiated as well.

- Conversion of unsecured loans: Unsecured loans are loans taken without any collateral or security. They have a higher interest rate due to higher risk. Notify banks about your financial crisis and get your unsecured loans converted to secured loans by offering security. It will lower the interest rate as well as the EMI burden.

- Seek professional counselling: This should be your last resort or first choice depending on how you look at it. Negotiation is an art, and you need to be a master while dealing with a prestigious entity such as a bank. Most people are not even able to request for a negotiation confidently, let alone toil with the banks about terms and conditions. Besides, the legal expertise of most loan borrowers is limited. Hence, approaching a debt counselling agency like Credit Monitor, who has an established relationship with the banks can get you an easy entry and settlement. We don’t charge a rupee from our customers, and all our debt counselling services can be availed free of cost. You’d be pleased to know that we’ve helped more than two thousand people become debt-free at no additional charge!

Now that you are aware about your powers than most defaulters in our country will ever be, initiate a conversation with your bank, or Credit Monitor, whomever you are comfortable with. Negotiation is hard, but a life full of debt and stress is harder! Be more responsible for your financial life. Get in touch with a concerned authority to discuss your debt at earliest.